High Deductible Medigap Plan G - 70% Cheaper Premiums

In 2025, we saw some of the highest Medicare Supplement rate increases in the history of the industry. I've been in the Medicare business for over 15 years, and even I have never seen rate increases this high.

Historically, rate increases range from 5 to 7%, but in 2025, we saw rate increases as high as 40% in states like Illinois and 25% in various states across the US.

Today, I want to show you a plan that's been hiding in plain sight - which can help you combat the rising costs of the standard Plan G and Plan N, while giving you the same great features of all the benefits of Medicare Supplement plans.

I've been helping people understand how Medicare works and Medicare Supplement insurance for over 15 years. And today I want to dive into a plan that some people know about, some people are afraid of, and some people don't quite understand, and that is the High Deductible Medicare Supplement Plan G.

I'm going to break down:

- How High Deductible Plan G works

- Show you the similarities between Plan G vs High Deductible Plan G

- How they differ significantly in price

- How much each of these plans will cost you over the years

So, let's get started.

Key Takeaways

Before we get started, the very most important thing you need to understand is that the benefits on standard Plan G are the exact same benefits as the High Deductible Plan G. Both laid side by side, one is not going to give you more medical coverage than the other one.

The difference is how exactly you are going to pay, whether it's per month on a higher premium with standard Plan G or a percentage of the medical claims when you use the High Deductible Plan G (with a lower premium than standard Plan G).

Definitely keep in mind that there are no lesser benefits with either plan. The benefit coverages are identical.

Another big takeaway when you're considering High Deductible Plan G: your traditional Medicare Part A and B are always in place first and the structure of those benefits doesn't change. Medicare Part A and B will still pay on your behalf according to their medical coverage before the High Deductible Plan G comes into the picture.

So, let me say that a different way. Most people think that before they'll get any medical coverage from Medicare or the High Deductible G Plan, they have to pay the High Deductible first, which in 2026 is $2,950. That is not true.

And I'll show you some real-life examples of what it would cost you to go to the doctor, have medical testing done (or a hospital stay), and I'll show you exactly what you could expect to pay in the same scenario if you had either one of the plans.

Plan Benefit Comparison

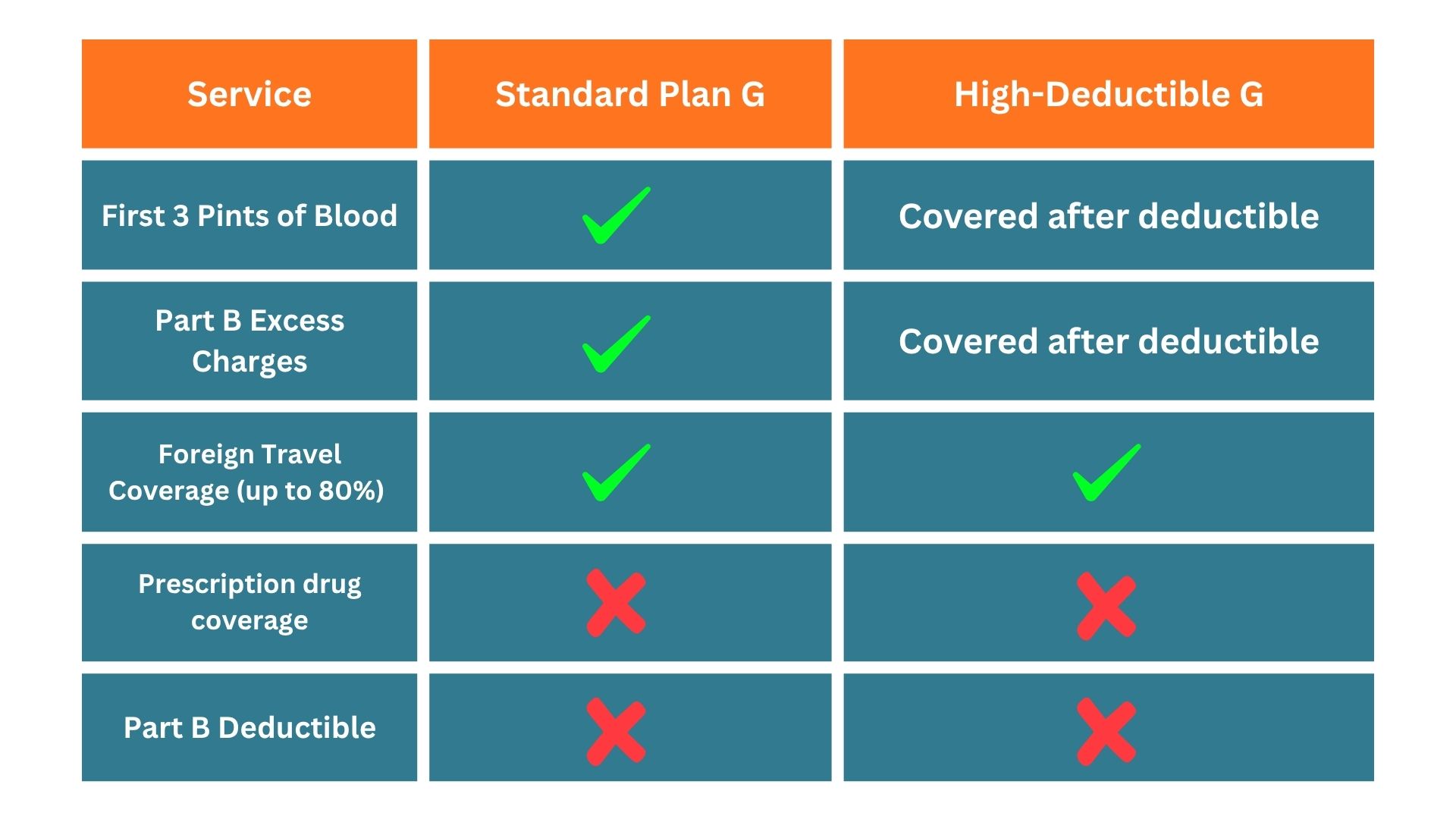

This is a standard chart that CMS puts out with your services, including your Part A inpatient, your Part A deductible, skilled nursing, hospice care, and Part B co-insurance.

Basically the chart you've seen floating around that shows covered services actually looks very confusing. I put this new chart here to show you that the standard Plan G covers those services. The High Deductible Plan G covers those services after the deductible, and as we continue on, it will make more sense.

We've got the first three pints of blood, Part B excess charges, foreign travel up to 80% (up to plan limits). Both are going to cover those. Neither will cover prescription drug benefits or the Part B deductible.

Now, the prescription drug benefits I'm referring to are prescriptions your doctor prescribes. If you are going to receive any type of medical injection in the doctor's office, it's covered on both plans.

For your standard maintenance medication, you would need a standalone prescription Part D plan, which would be applicable to both the High Deductible G and their standard G. So again, they are exactly the same in that area.

Both plans include all of the same features, including:

- No networks

- No prior authorizations

- No annual benefit changes

- Freedom to travel

- Guaranteed renewable

- Specialty facilities anywhere in the country

All of those features are identical with both of the G plans.

Out Of Pocket Examples

Let's get into out-of-pocket examples. I will warn you - I put together the real-life scenarios, but Original Medicare is quite complicated in the way that the benefits work.

So, I tried to put the charts together in as easy to read fashion as possible.

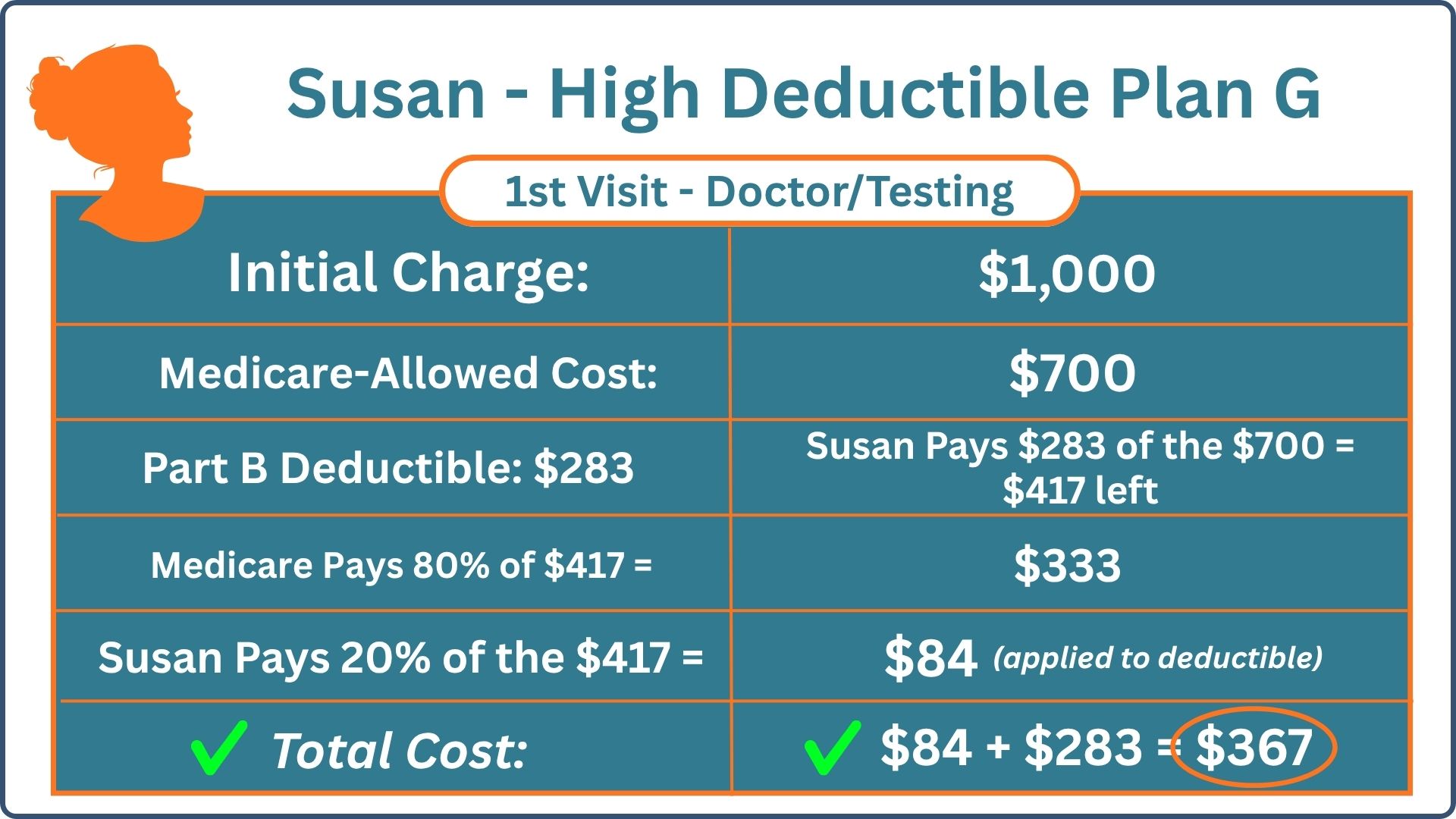

We're starting out with Susan. She has the High Deductible Plan G, and we are making sure that this is an example of her first visit of the year. She hasn't incurred any medical care yet. This will be her first visit, and we'll say that this is for an outpatient office visit with some minor testing.

We have an initial doctor visit charge of $1,000. Medicare allowable amount is based on the negotiated rates. Medicare says, "We only allow 700 for that, so the provider honors the $700."

So first, we have your Part B deductible of $283, and the remainder is $417. Medicare will pay 80% of that $417 bill, which is $333. You pay 20% of that $417 bill, which equals $84. That $84 is applied to your High Deductible Plan G deductible.

The Part B deductible does apply to your High Deductible Plan G. It is a once-per-year deductible. So, in this scenario, your total cost would be your $84 for your 20% plus your $283. So, in that real-life scenario, you're looking at a total of $368.

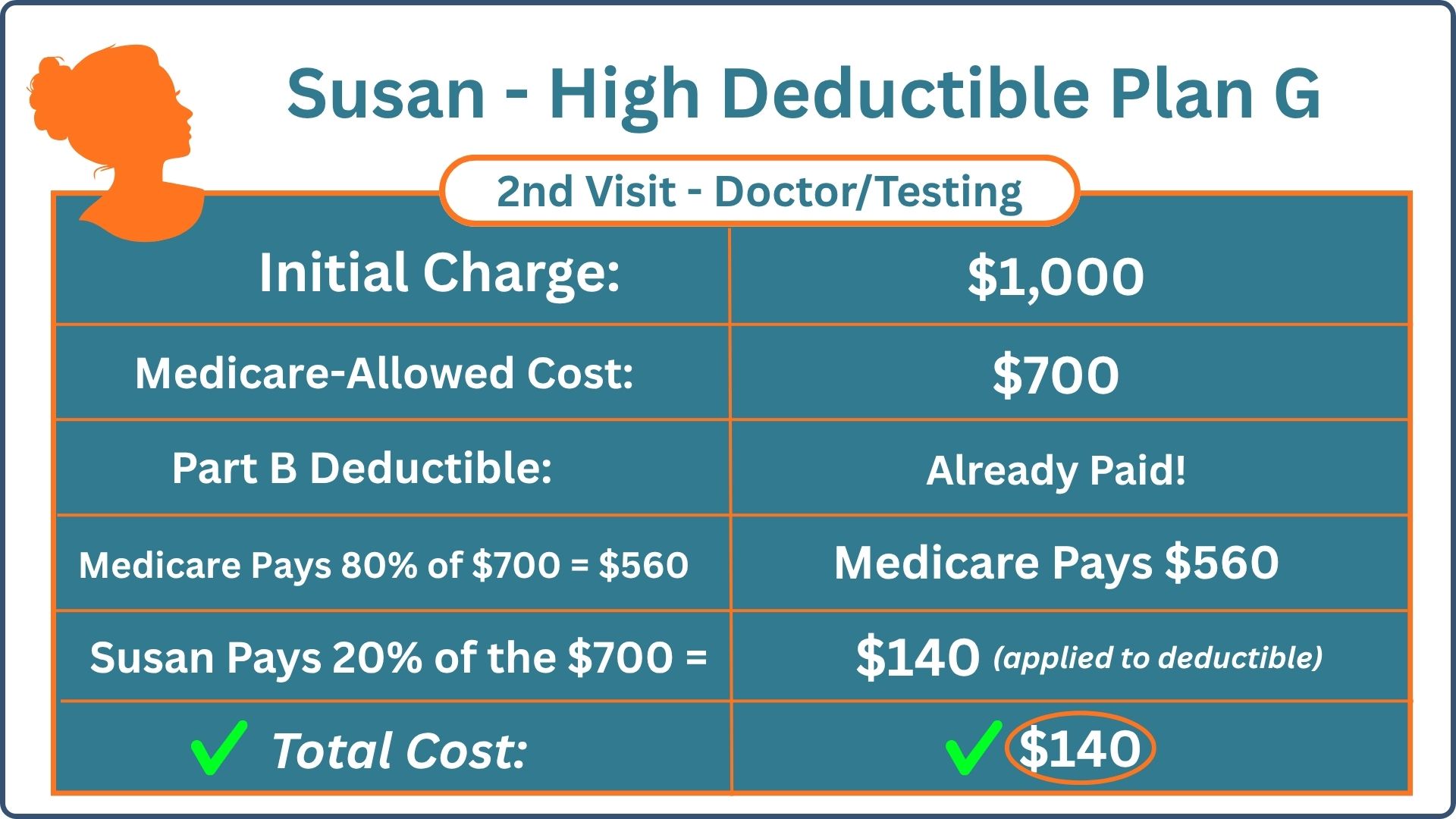

Here we have Susan with her second visit using the same metrics on the High Deductible G.

The initial charge is $1,000. Medicare allows $700, and because Susan paid her Part B deductible in the first visit, that means that deductible is taken care of for the calendar year.

So now, we have a $700 bill. Medicare pays 80% of that, which means they'll pay $560 of that bill.

Susan will repay 20% of that $700 initial bill, which equals $140. That $140 is applied or subtracted from the High G deductible. So, the total cost in this second visit for Susan is $140.

Remember, Medicare is made up of Part A and B. So, in this scenario, we're talking about basic outpatient care falling under the Part B.

And again, remember, the percentages that you're paying on your Part B in the first and second example are going to be subtracted from your total High Deductible G amount.

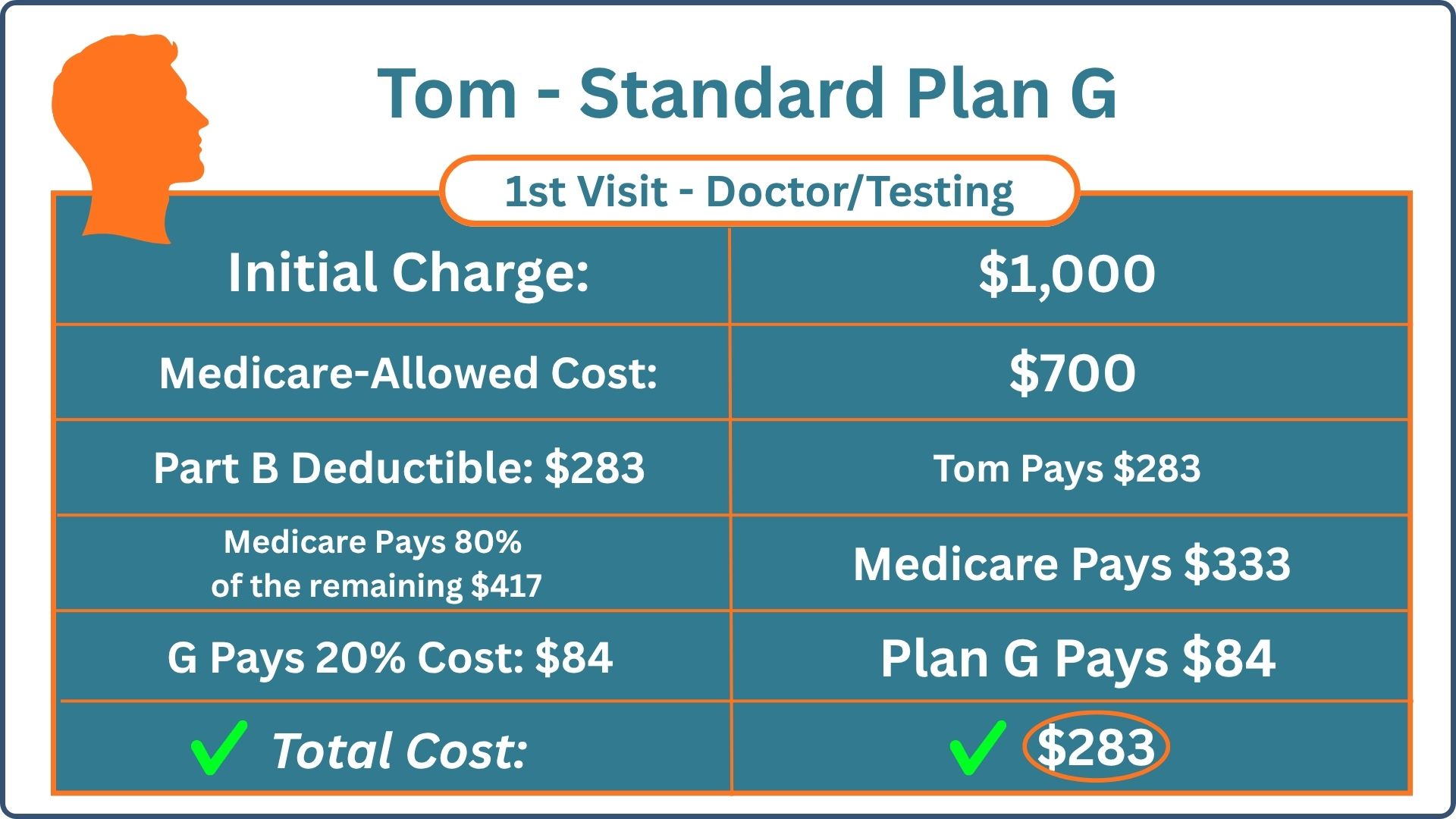

Now, moving on to the same scenario with standard Plan G, we have Tom with the initial charge of $1,000. Again, Medicare allowed cost is $700, so now you have a $700 bill left.

You are going to immediately pay your Part B deductible, which is the $283. That still applies in this standard Plan G scenario. So, you're dealing with $417 left after you paid that Part B deductible.

Medicare is going to pay 80% of that remainder, which is $333, and here the standard Plan G is going to come in and pay the remaining 20% cost, which covers the remaining $84.

So, Plan G in this scenario picks up that 20% for you, where the High Deductible Plan G does not until that deductible is satisfied. So, in the standard G scenario, Tom is only going to pay $283 for that first visit.

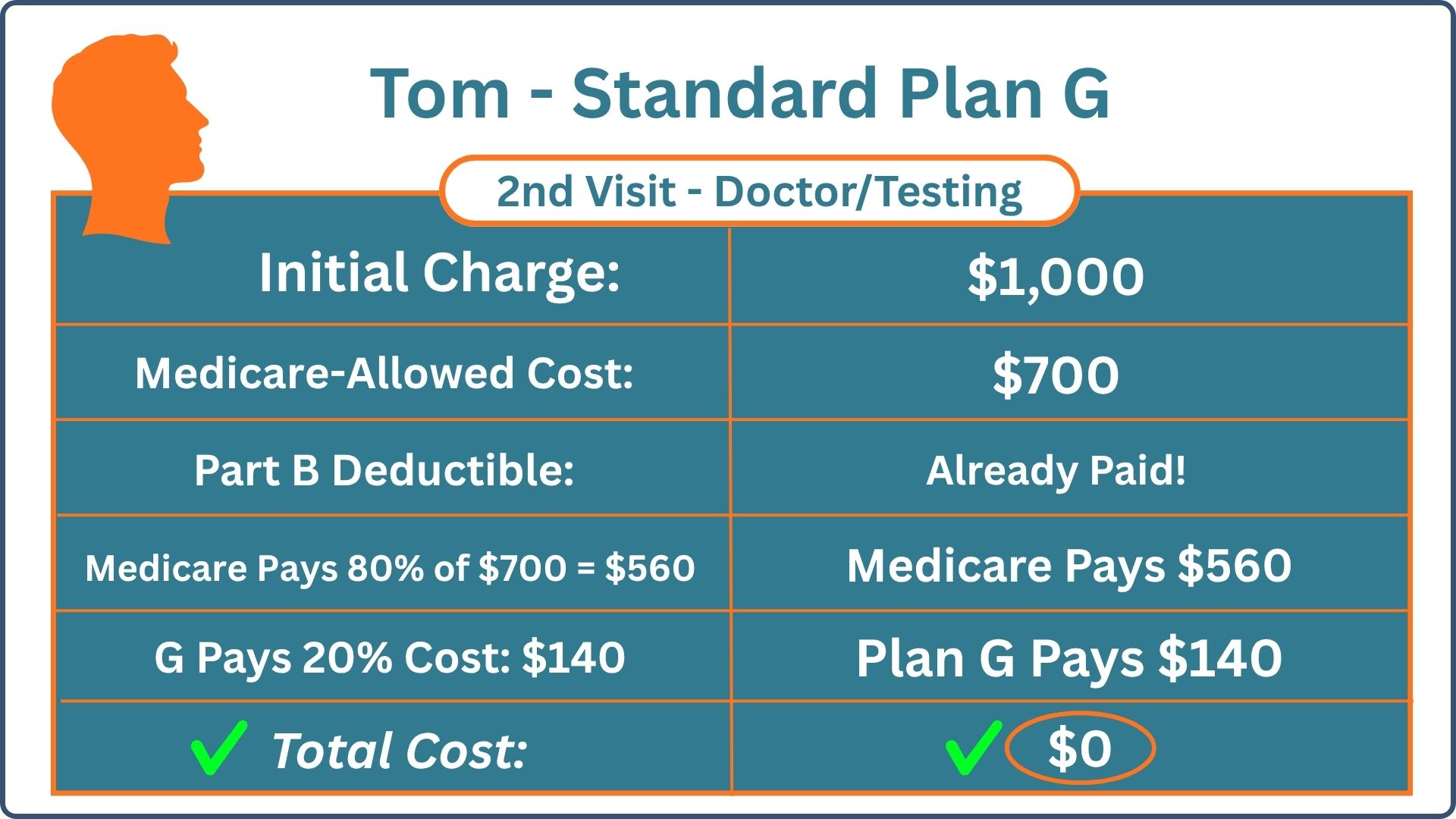

Moving on to the second visit that Tom experiences with standard Plan G. We're working with the same number as $1,000 initial charge, Medicare allows $700, and here's the big difference: since you paid the Part B deductible in your first visit, it's now satisfied for the calendar year.

So, we're looking at a remaining bill of $700. Medicare pays 80% of that $700 bill, which equals $560. Plan G steps in and pays the 20% cost of the remaining $140.

So, in this scenario, Plan G pays the remaining $140 for you, making your total cost for the second visit $0.

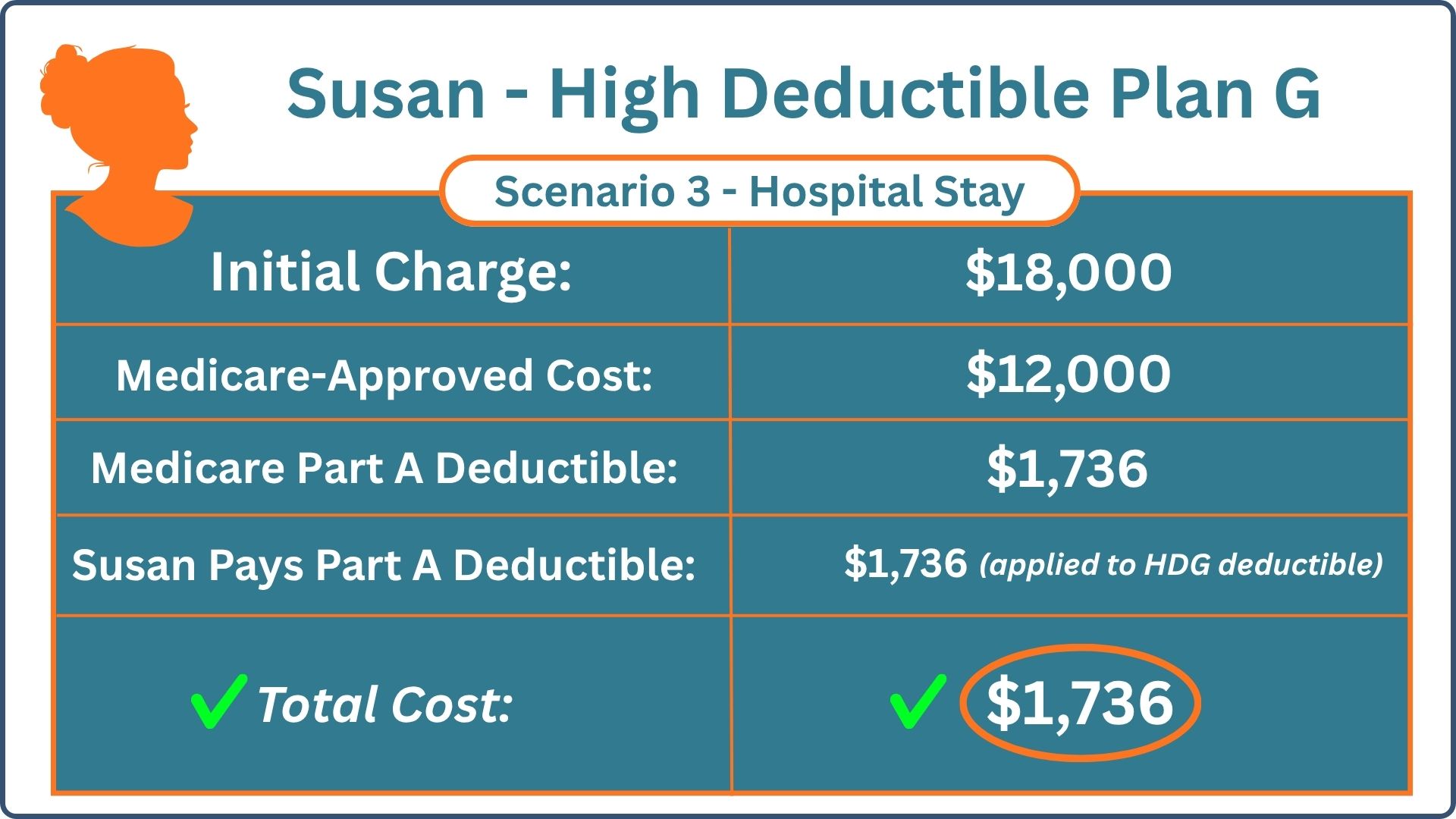

The next scenario is Susan again on the High Deductible G with a hospital stay. So, let's say the hospital charges are $18,000, Medicare approved cost is $12,000.

Now that we're onto Part A hospitalization, you aren't really too concerned about the Medicare-approved amount because you're not dealing with the 80/20 rule here.

You've got your Medicare Part A deductible, which is $1,736 for 2026. This would be your out of pocket for that $18,000 hospital stay. The $1,736 would also be applied to the High Deductible Plan G.

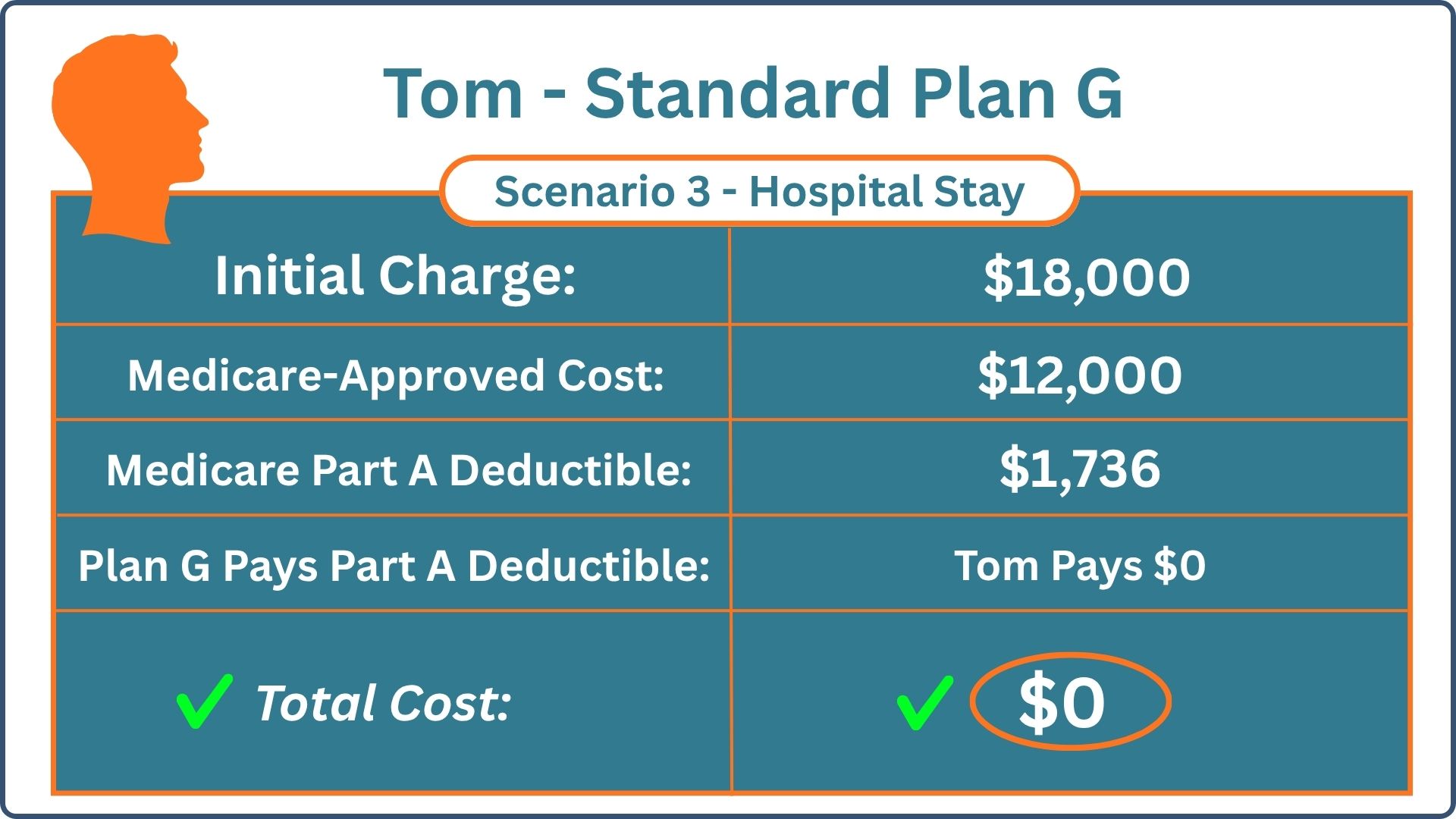

Moving on to Tom in the next scenario, he's in the hospital with his standard Plan G, The total is $18,000, Medicare approved $12K, the Medicare Part A deductible is still there.

Now, here's the difference. The Plan G pays that Part A deductible. So, in this scenario of a hospitalization Tom is coming out at no cost. This is an example of the real difference between High Deductible Plan G and Standard Plan G.

The biggest takeaway here is remember the features of your Medicare Part A and B are happening immediately. So, whatever your coverages are for your Part A and B, they're immediate, they're not sheltered behind that High Deductible Plan G deductible.

Why High Deductible Plan G Is So Appealing

In the health insurance world, High Deductible Plan G is very attractive if you know what you're looking for.

As an example, my wife, two kids and I are on an individual family plan, and our monthly premium is now $1,400. We have a $5,000 deductible before Blue Cross will pay anything. So, I'm paying $1,400 a month, and they won't pay anything until I've satisfied $5,000. That's incredibly absurd in my opinion.

When you're looking at Original Medicare A and B, one of the risks is that there's no cap on your 20%, also mulitple hospital stays can mean multiple Part A deductible (per benefit period).

So, if you have Original Medicare A and B only, there's no cap on your 20% or the areas of Medicare where you have shared costs. That could just go on forever if you had a catastrophic situation.

When you put High Deductible Plan G on top of your Original Medicare A and B, it's a phenomenal option because Original Medicare is still working on your behalf immediately and then you have that out of pocket limit on the High Deductible G.

Basically, when you put these three together, it's as though you have Original Medicare A and B with an out-of-pocket maximum of the $2,950. Couple this with the premium savings over Plan G and Plan N and it will be even more enticing

A lot of people will give you advice, "Well, you know, find a company that doesn't close their block of business and skyrocket the premiums," or "Find a company that is brand new and offers lower rates."

I'm here to tell you that there are no secret low-premium risk pools for the standard Plan G and Plan N.

Whatever company you pick, whatever company you're looking at, you're going to find, obviously find your lowest premium, but premiums are going to increase. So, knowledge is power. Once you understand the inner workings of how standard G and High G work, it empowers you to say, "I confidently understand now how these two work. I'm either not comfortable with the High Deductible G, and I'd rather just pay the Standard G premium," which is perfectly fine.

I'm not here to say that standard Plan G is bad, and you need to go do away with it. I'm simply presenting you with a creative solution that gives you all the same freedom and flexibility of the standard Plan G at a much lower premium.

Use those examples to help build cost analasyst in your brain of things you've gone through in the past, or maybe you had a surgery or treatment, you can look back and say, "Well, I did this and this. What would my cost have been if I had the standard G?" or "What would my cost have been if I had the High Deductible?"

In the scenario that you or your spouse just walked through, it will give you a number to work with, and then you could say, "Well, if I had one of these plans back then, which avenue would I feel the most comfortable with?"

And that really is what it boils down to is again, knowledge is power. Once you know the way both avenues work, you can confidently pick one or the other.

Price Comparisons By State

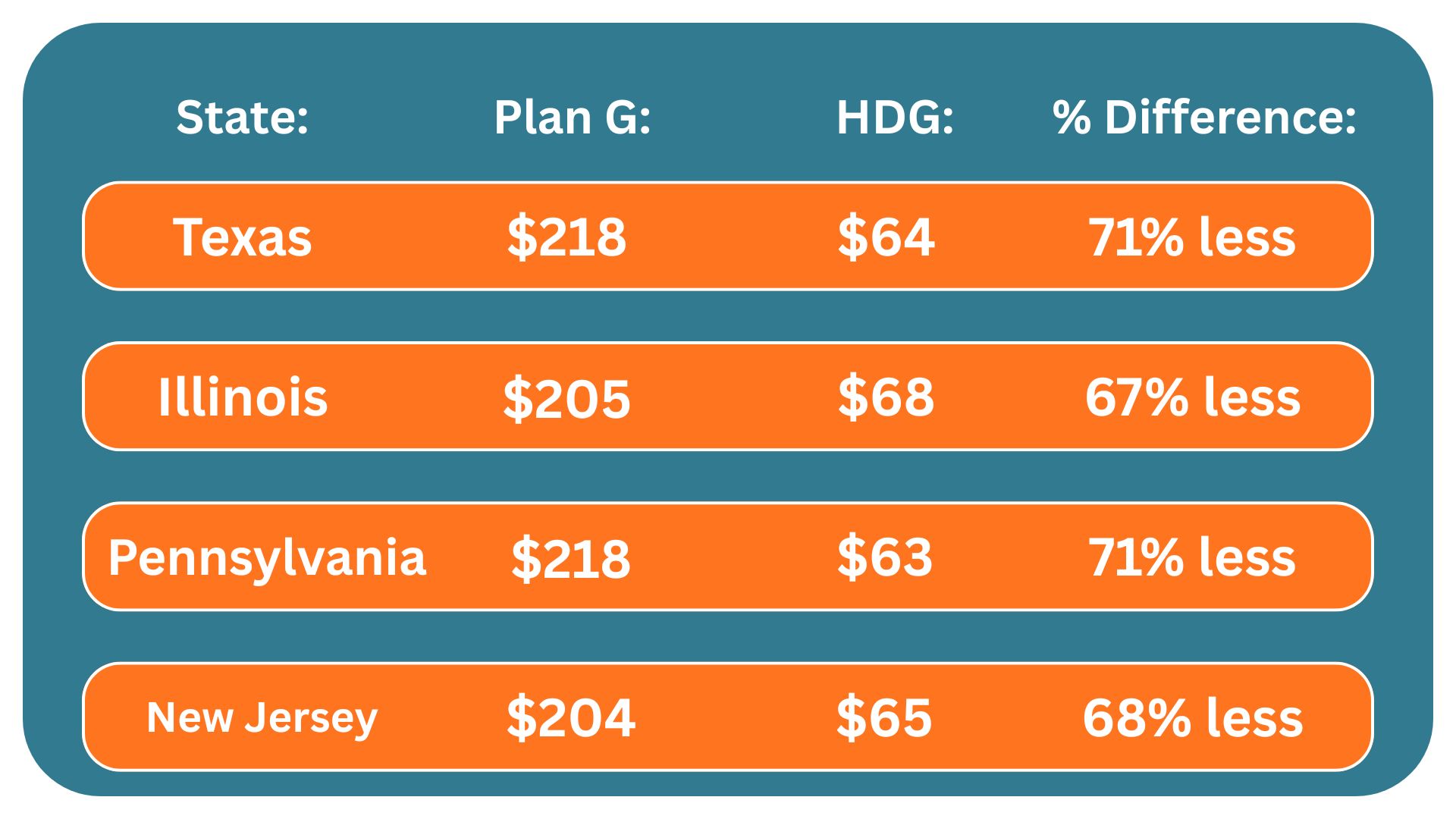

Let's get into some premiums now, and I'll show you the stark contrast between the High Deductible G and the standard Plan G. So, I've put together a list of some of the largest states based on population.

These averages should withstand averages in different pockets of the country. So, I'll draw out the most expensive, highly populated states first, and then I'll show you some mixed in smaller states in the Midwest.

This will give you a gauge on what you can expect on the standard and High G.

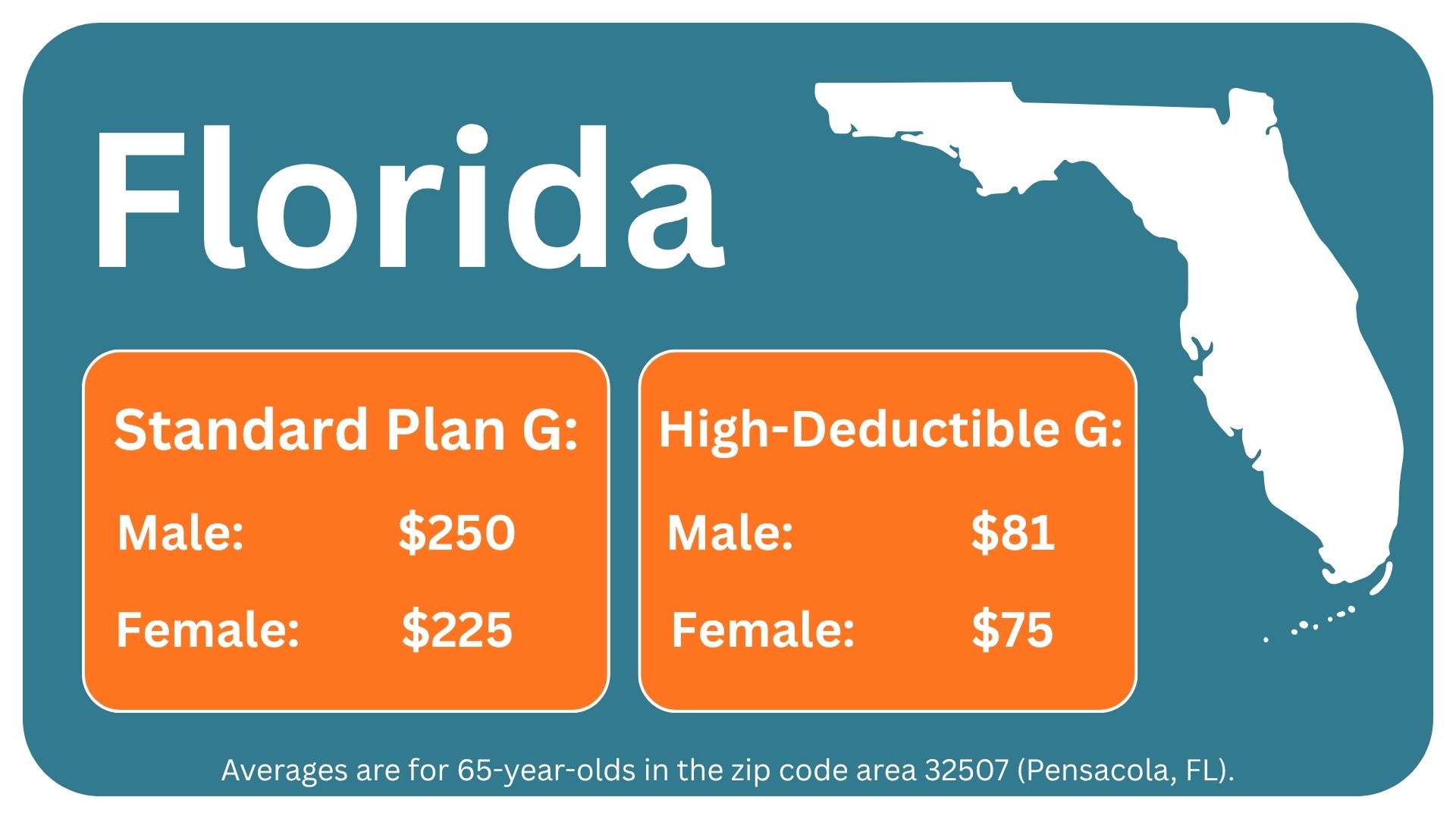

Starting off, we're looking at Florida. This is for a 65-year-old in Escambia County, which is in Pensacola, Florida.

This again is just an example.

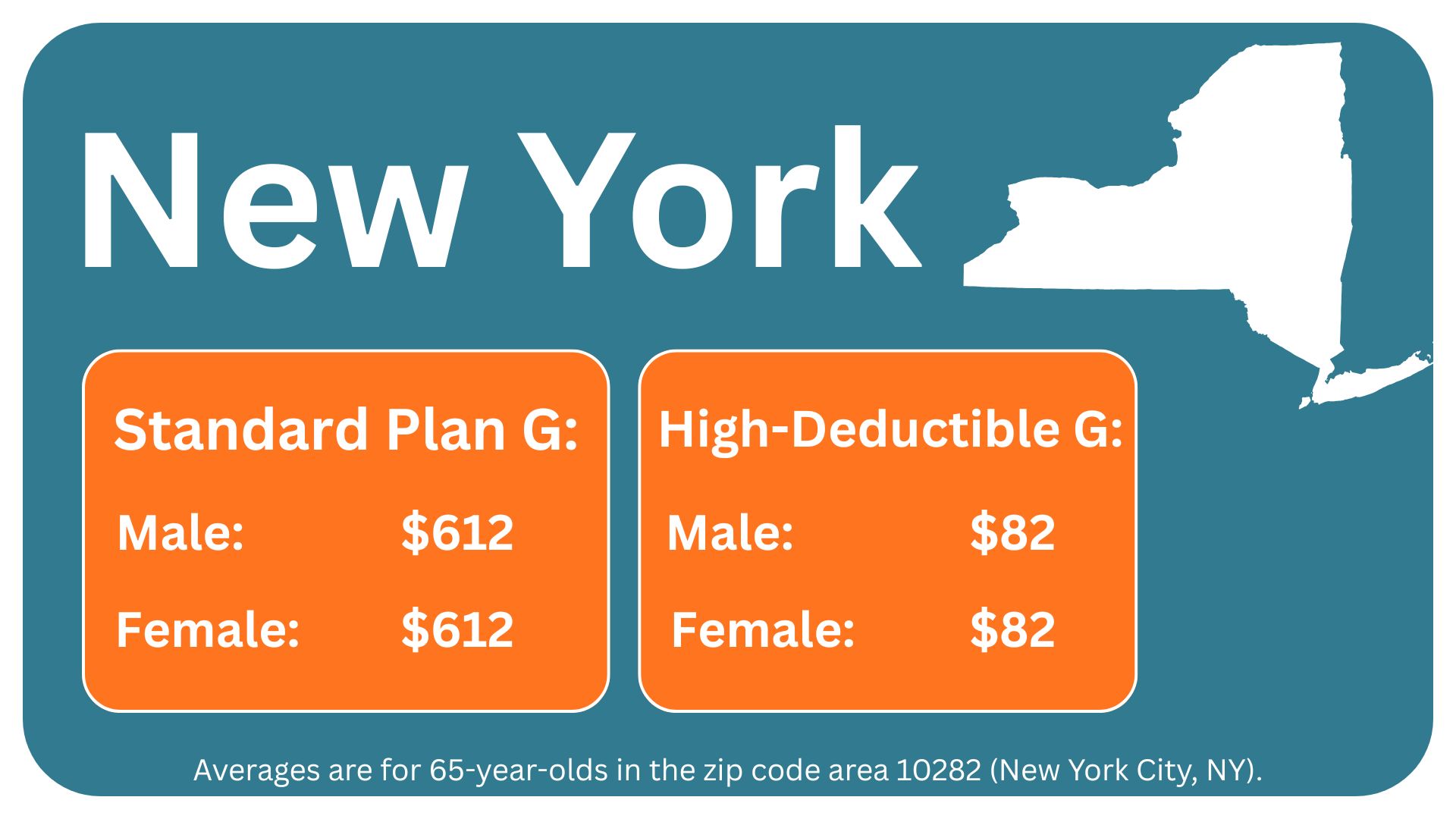

Moving on to New York, which is probably the most expensive state in the country.

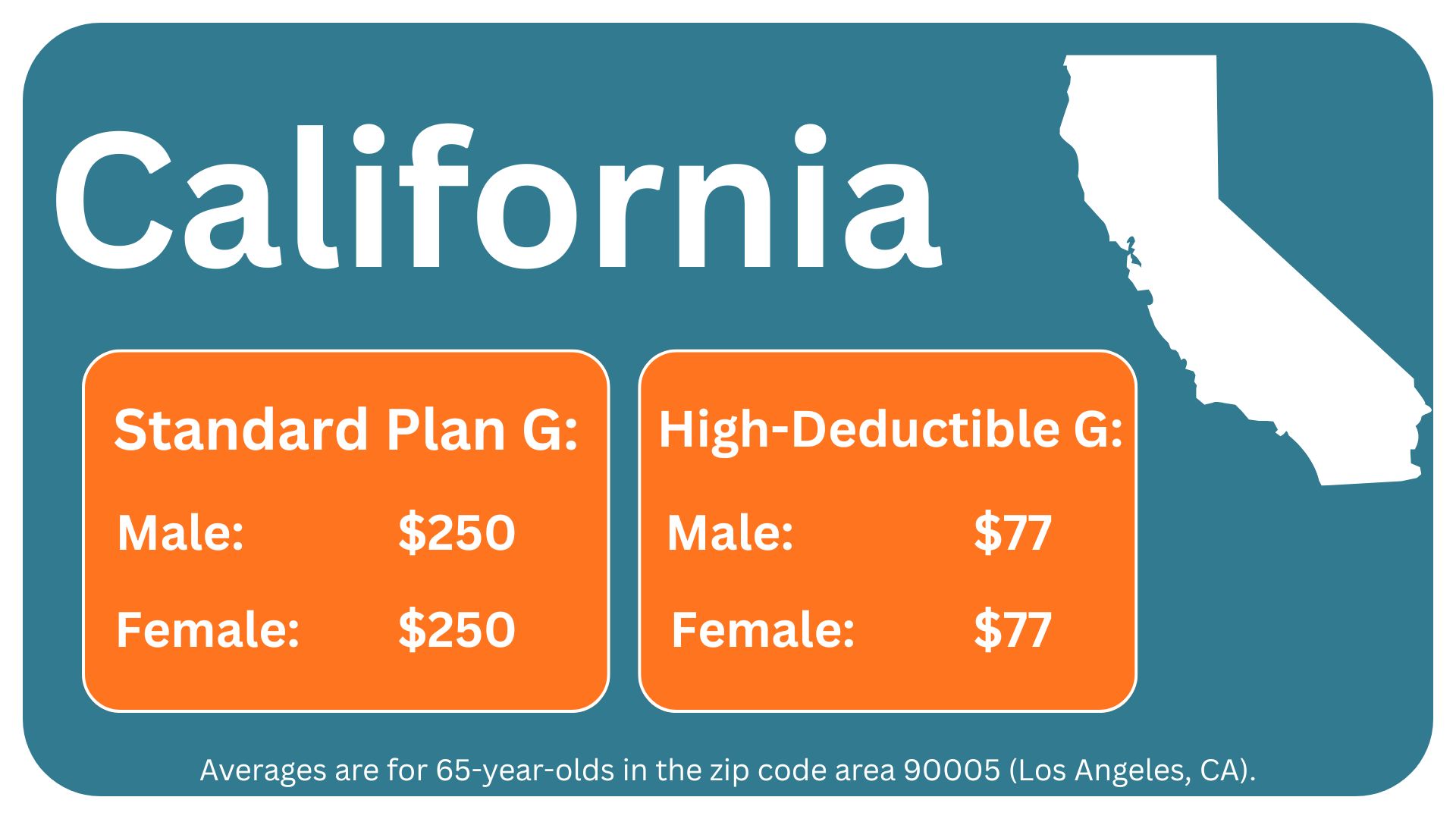

Moving on to California, we're looking at standard Plan G is $250 for either male or female. High Deductible G is $77 for either.

And then as we get into some of the smaller states, you can see we're averaging around 70% cheaper premiums for the High Deductible Plan G.

So again, in the beginning, you may have been, "Well, I'm nervous about paying that Part A deductible for a hospitalization on the High Deductible G," but you can see here you are either going to pay at time of service if you have the High Deductible G, or you're going to pay in the monthly premium.

So, there simply is no way to get away from paying something.

Do you want to pay ahead in advance with the standard Plan G and be done, or would you rather save the monthly premiums and pay as it comes with the High Deductible G?

What About Deductible Increases?

So what is going to happen to the deductible on High Deductible Plan G? What if it increases too high?

The honest answer is that we cannot predict the future. But I have put together the most relevant historical deductible increases I could find for High Deductible Plan G, going back to 2021.

Here is what the yearly deductible increases have looked like:

Based on the historical data, you are looking at deductible increases that have mostly been in the 3% to 4% range, with a couple of higher years.

Now, you could look at that and say, “Well, that scares me.” And that is fair. But your premium is also going to increase on a standard Plan G. So again, this comes down to a trade-off. Which camp do you want to be in?

Five-Year and Ten-Year Premium Cost Estimates

Now let’s get into the five-year total premium cost for standard Plan G and High Deductible Plan G. Starting with High Deductible Plan G, your estimated five-year premium cost is anywhere between $3,700 and $4,100. Your estimated 10-year premium cost is around $7,500 to $8,200.

Again, we are talking about the monthly premium here. We are not talking about the deductible or your out-of-pocket costs. On a standard Plan G, the estimated five-year premium cost is around $12,000 to $13,000. The estimated 10-year premium cost is around $24,000 to $26,000.

If you stop and think about this for just a moment, the standard Plan G premium is the guaranteed amount you are going to pay if you have that plan. On High Deductible Plan G, the premium is the minimum amount you are going to pay for your medical care.

If you do have claims, obviously, your out-of-pocket costs are going to be added to that.

So, with standard Plan G, there are virtually no other out-of-pocket costs, but the premium is significantly higher. With High Deductible Plan G, your raw operational cost is significantly lower until you use the plan. Again, that is another feature to weigh long term.

Historical Rate Increases

Moving on to historical rate increases. As I mentioned earlier, standard Plan G has had some of the highest rate increases in history, ranging from 20% to 45% in some cases. The average rate increase on High Deductible Plan G has been closer to 3% to 5% per year.

Let me stop and point something out. When you are talking about a 20% to 40% increase on standard Plan G, you are talking about that percentage being applied to an already higher amount. If you are starting at $200 per month and you get a 20% rate increase, that is a $40 per month increase. That is almost $500 more per year.

Now, if you are on High Deductible Plan G and your premium is $70 per month, a 10% rate increase is $7. If your High Deductible Plan G premium is $100 per month, a 10% increase would be $10. So, because you are starting so low, a premium increase can be much smaller in actual dollars because you are dealing with a percentage of such a small number.

That is the point. Neither plan is better than the other. I just want you to understand how both options work.

High Deductible Plan G vs. Medicare Advantage

I would love to see somebody on High Deductible Plan G over a Medicare Advantage plan any day of the week. Why? Because with a Medicare Supplement plan, you do not have the same concerns about your plan being canceled, your network changing, or your doctor no longer being in network.

That does not mean High Deductible Plan G is perfect. You still need to understand the deductible, the premium, and your possible out-of-pocket exposure. But if you are comparing High Deductible Plan G to Medicare Advantage, I would much rather see someone keep the freedom and stability of a Medicare Supplement plan, even if it is the high deductible version.

So, what happens if the High Deductible Plan G deductible keeps increasing? It may increase. We cannot predict the future. But based on historical data, the increases have generally been manageable. At the same time, standard Plan G premiums can also increase, and those increases are applied to a much higher monthly premium.

Again, this is a trade-off. Do you want the predictability of standard Plan G and a higher monthly premium? Or do you want the lower monthly premium of High Deductible Plan G and accept that you may have more out-of-pocket cost if you use the plan?

Final Thoughts

The beauty of both supplements is all of the freedom and control that you have over your care because imagine if you have the High Deductible Plan G and you don't have a hospitalization for five years. Well, that's a significant amount of money you've saved in claims and premiums.

As you review this information, take your time and go back through any areas that may need a little more attention. Some parts of Medicare Supplement planning are easier to understand after you look at the numbers more than once, especially when comparing premiums, deductibles, rate increases, and long-term costs.

If you need help, you can give us a call. We can walk you through a needs analysis, which means we take your specific situation, compare your options, and help you understand which plan may be the most suitable fit for you.

FAQ

High Deductible Plan G is a Medicare Supplement (Medigap) plan that provides the same core benefits as standard Plan G after you meet the annual deductible. In exchange for taking on more upfront out-of-pocket responsibility, the monthly premium is often significantly lower than a traditional Plan G premium. For many healthy Medicare beneficiaries, it can be a way to reduce monthly insurance costs while still maintaining protection against large medical expenses.

In many areas, High Deductible Plan G premiums can be 50% to 70% lower than standard Plan G premiums. The exact savings depend on your age, ZIP code, gender, tobacco status, and the insurance company you choose. While the monthly premium is substantially lower, you should compare the premium savings against the annual deductible to determine whether the plan makes sense for your situation.

Yes. Once the annual deductible has been satisfied, High Deductible Plan G provides the same Medicare Supplement benefits as standard Plan G. The difference is not the coverage itself but when the coverage begins paying. Standard Plan G starts paying its share immediately after Medicare and the Part B deductible, while High Deductible Plan G requires you to satisfy the annual high deductible before the plan begins covering eligible expenses.

High Deductible Plan G is often a good fit for people who want lower monthly premiums, do not visit doctors frequently, have savings available for unexpected healthcare costs, or simply prefer to self-insure smaller expenses in exchange for lower ongoing insurance costs. It can also appeal to retirees looking to reduce fixed monthly expenses while still maintaining protection against catastrophic medical bills.

It depends on your healthcare usage, budget, and risk tolerance. For some people, the premium savings can far exceed the amount they spend on out-of-pocket medical costs, making High Deductible Plan G an excellent value. For others who prefer predictable healthcare expenses or expect frequent medical care, a standard Plan G may be the better choice. The best way to determine which option provides the most value is to compare both the monthly premium and your potential annual costs under each plan.

Or enter your zip code to shop online